Affordability Is Personal Yet Also Lender-Defined

Affordability has two dimensions. First, there’s your own definition of what feels manageable month to month. Then there’s the lender’s view, based on a strict set of criteria. These two perspectives don’t always line up—and that’s why it’s so important to look at both.

What you feel comfortable spending will depend on your lifestyle, priorities, and long-term financial goals. Lenders, on the other hand, focus on risk: they want to ensure that your mortgage payments will be sustainable not just now, but in the future.

Start with Your Budget, Not the Asking Price

Before looking at properties or applying for a mortgage, it’s worth taking a closer look at your own finances. What’s realistic for you to spend each month without overextending?

A useful starting point is the 28:36 rule:

- No more than 28% of your gross monthly income should go toward your mortgage (including interest and principal).

- No more than 36% should go toward all debt repayments combined—including your mortgage, credit cards, car loans, and any other finance commitments.

For example, if your gross income is £3,000 per month:

- Your ideal mortgage payment would be around £840.

- Your total monthly debt obligations would ideally stay under £1,080.

That said, these percentages are just guidelines. Everyone’s financial landscape looks different. A more accurate approach is to create a detailed budget planner that includes:

- Day-to-day living expenses

- Lifestyle spending (hobbies, dining, entertainment)

- Savings and emergency funds

- Holiday plans

- Future one-off expenses

Once you have a clear idea of your ideal monthly mortgage payment, you can use online calculators—or speak to a mortgage adviser—to estimate what that might translate to in borrowing terms.

To make this easier, you can download our free budget planner to map out your income, expenses, and potential mortgage payments before approaching lenders.

How Lenders Calculate Affordability

While your budget tells you what you want to spend, a lender will run their own affordability checks to decide what they’re willing to lend you.

Most lenders start with a loan-to-income multiple, which can range from 4 to 6 times your gross annual income. However, this is just a cap—not a guarantee. The Prudential Regulation Authority’s guidelines outline these multiples to ensure responsible lending practices.

From there, they look more deeply at your financial situation to assess whether the proposed mortgage is truly affordable based on their criteria.

According to the latest mortgage lending statistics from the Financial Conduct Authority (FCA), understanding these criteria is crucial for prospective borrowers.

What Lenders Consider When Assessing Your Application

Affordability assessments vary slightly between lenders, but most take the following into account:

- The loan amount and mortgage term

- Number of applicants and any dependents, including both children and adults

- Your current loan commitments, such as car finance or personal loans

- Student loan repayments, especially those deducted at source

- Credit card balances and outstanding debt

- Ground rent and service charges for leasehold properties

- Childcare costs or private school fees, if relevant

Some lenders will also look at regular household expenses like groceries, utilities, and transport. Many now use Office for National Statistics (ONS) figures as a baseline for these categories, rather than digging into your individual spending habits.

Another important point: lenders assess your ability to repay the mortgage using stress-tested interest rates, not just today’s rate. This means they factor in higher hypothetical rates to ensure your repayments would still be affordable if interest rates rise.

Why Mortgage Offers Can Vary So Widely Between Lenders

Lenders don’t all interpret affordability in the same way. That’s why it’s not unusual to receive very different offers depending on who you speak to.

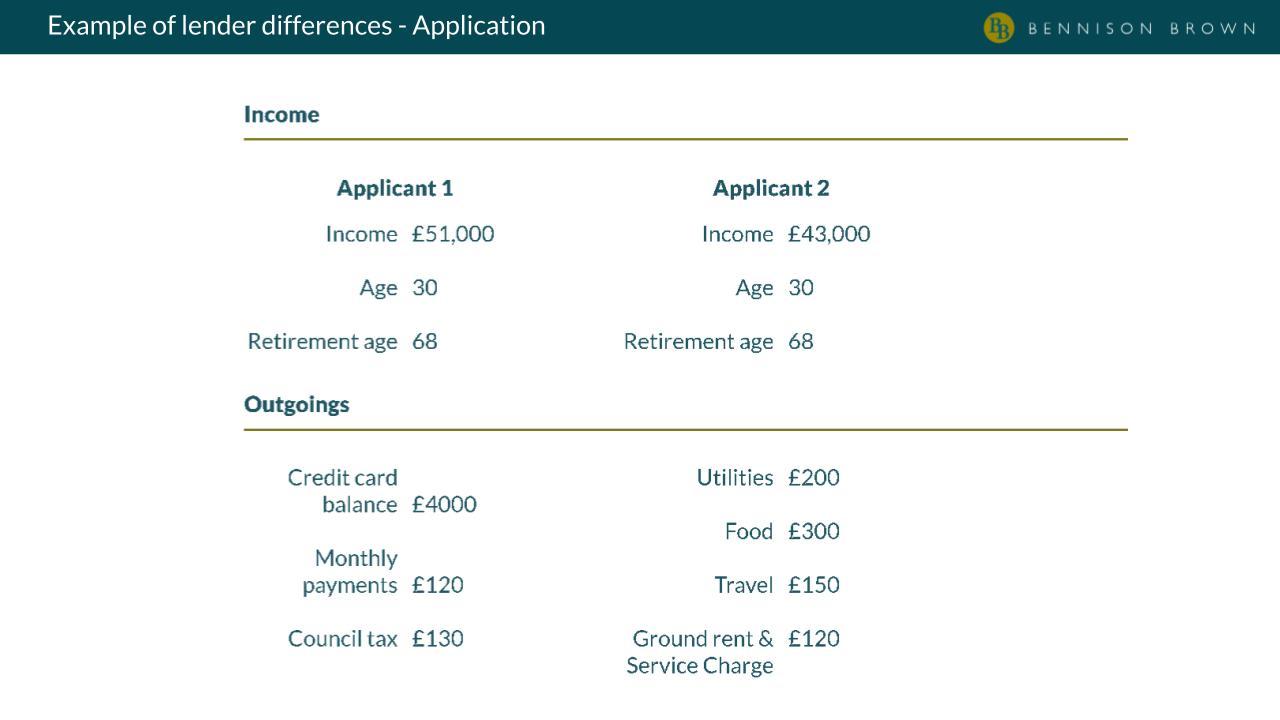

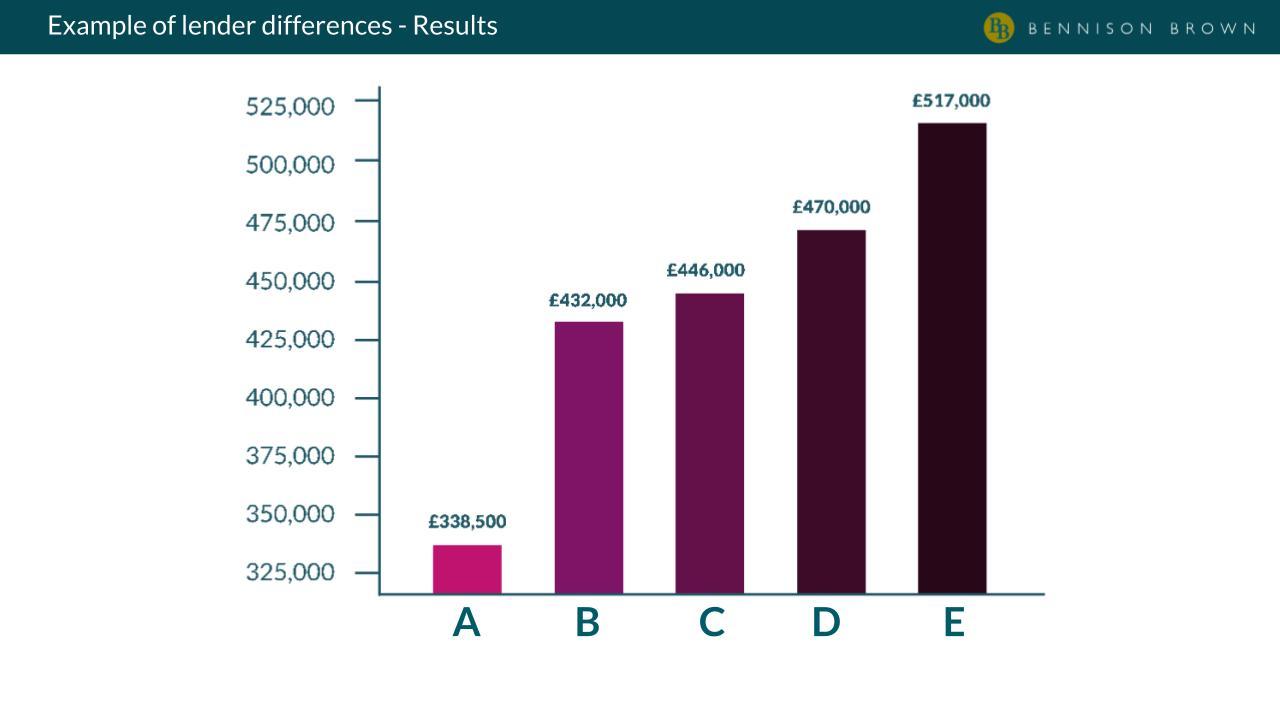

For example, we recently reviewed the case of a couple in their early 30s earning £94,000 combined. They had a £4,000 credit card balance and were looking to buy a flat with a £120/month service charge. Some lenders offered them a mortgage of £338,000, while others were willing to lend up to £517,000—a £179,000 difference.

This kind of variation shows just how important it is to compare options—and why working with a whole-of-market broker can be so valuable.

Our research found that mortgage offers can vary significantly between lenders, even for the same applicant. For a real-world example of how lender decisions differ, check out this breakdown.

Example of lender differences – Application

Example of lender differences – Results

Just Because You Can Borrow More Doesn’t Mean You Should

Sometimes, your budget and the lender’s assessment will align. You may even find out that you’re eligible to borrow more than you initially expected.

But just because you can borrow a large amount doesn’t mean you should. It’s easy to get caught up in the excitement of a bigger home or a nicer area, but it’s important to stay grounded.

Stick to your original budget, and make sure your mortgage payments won’t leave you financially overstretched. Think about:

- Future changes in income

- Growing your family

- Maintenance and repair costs down the line

The goal isn’t just to buy a house—it’s to own a home that fits your life without compromising your financial stability.

If you’re unsure about how much you can afford—or how lenders will view your application—speaking to an experienced mortgage adviser can be a smart next step. They’ll help you understand your position and guide you through your options with clarity and confidence.

If you’d like expert support with understanding affordability or navigating mortgage calculations, feel free to contact Bennison Brown. We’re here to help you make sense of the numbers and find a solution that works for your budget and goals.